Developments in the national market, driven by retail players such as CVS, Walmart, and DaVita, have highlighted the fact that those who are seeking a competitive advantage in disrupting the current delivery of healthcare are not being limited by traditional boundaries, but are focused on the demands they’re hearing from consumers.

To compete successfully, the health systems of 10 to 15 years from now must be as different from their current form as existing systems are from the ones 80 years ago. In the past two decades, value-based reimbursement has moved forward, with the risk for the cost of care increasingly shifting to provider organizations, driven more by local employers and insurers than by Washington, DC.

So how do systems compete in the brave new world of value-based care? Differently. Very differently. Systems will need to focus on two critical drivers: patient centricity and value transparency.

Patient Centricity

When discussing patient centricity, we mean more than the patient experience or consumerism, though they’re both elements. A good patient experience is an outcome of true patient centricity. Too much focus on patient experience metrics can obscure the underlying transformation needed by implying that the end-user experience can be enhanced by just changing wall colors or providing valet parking. Real patient centricity is part culture, part infrastructure—and all by design.

From the “Build It and They Will Come” Model to a Competitive Marketplace

The real challenge is historical; most systems have grown out of a “build it and they will come” approach that long relied on the idea the hospital is the center of a set of services patients need and that they’ll have no choice but to go there for care. But even the physician office revolves around the provider, not the patient, in terms of schedule, location, and even physical layout. All of this must change in what has become an intensely competitive marketplace in which systems are vying for customers

A New Model for Patient Centricity

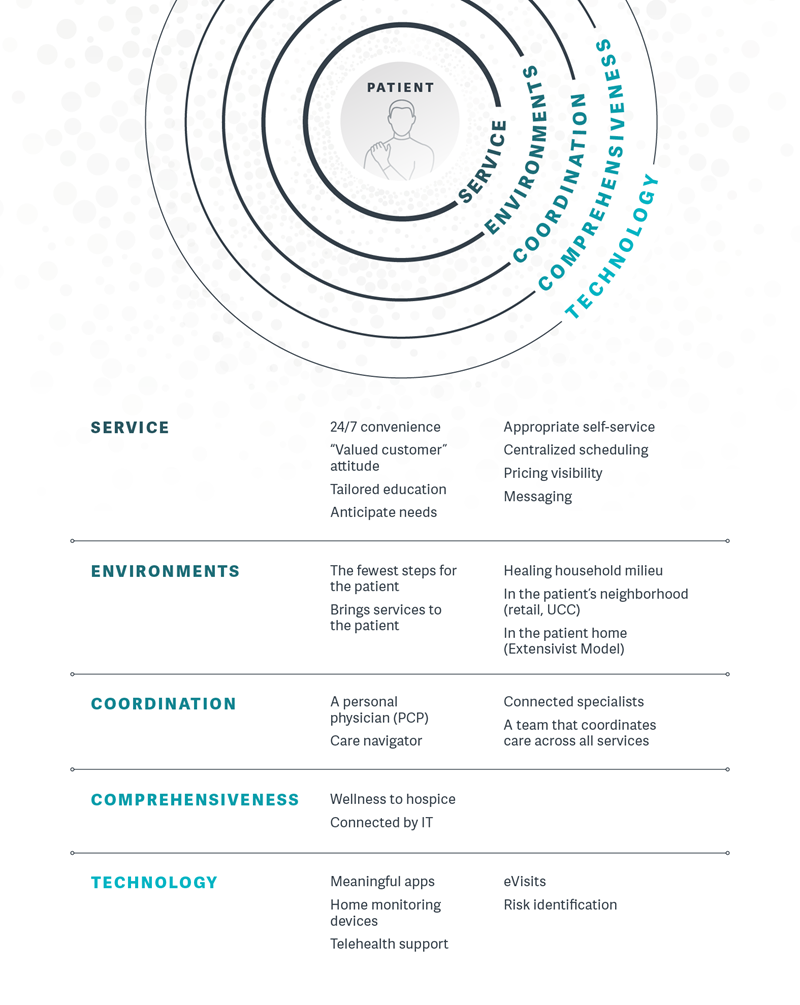

Patient centricity begins with a “valued customer” attitude, from the front desk of the hospital or physician office, to the physician, to the housekeeping and food service staff. This is more than an absence of rudeness or even an attitude of friendliness, but involves anticipating the needs of patients and meeting them, 24/7.

Though there are many elements to patient centricity, our view is that they can be organized into a concentric set of capabilities, each of which enables the other, beginning with service and ending with technology.

As if your business depended on them.

Though many of these elements seem intuitive, (just ask yourself if you’d rather go to a more patient-centric provider), there’s ample evidence that strategically putting them into place drives market capture.

Patient Centricity in Practice

One health system that increased its access to primary care by two hours each day saw a 9.4% boost in visits in just the first year, and 84% of patients surveyed would self-schedule visits if they could do so online.1 And this is merely tinkering with the status quo. If these relatively minor changes could have such an impact, imagine what true innovations across the system would bring. It’s no wonder that nonsystem retail clinics and urgent care locations have become a $10 billion industry in just the past five years.2

Value Transparency

Price Transparency as a Competitive Strategy

Price transparency as a competitive strategy becomes even more critical as payers and employers continue to increase patients’ exposure to costs, as Geisinger and Zoom Health3 have demonstrated. Research has shown that 82% of patients who compared prices across multiple providers would do so again, and 43% of those who have not yet tried to find price information say they would choose a less expensive doctor or facility if they knew the costs in advance.4

Even in a cash-only model, the Surgery Center of Oklahoma sees more patients from out of state and internationally since posting prices.5 There are innovative models emerging every day that provide not only transparency, but also financial enablement, to patients. A recent study showed that 25% of consumers put off care due to cost, and providers who offer financing have seen a significant impact on utilization.6 The market continues to be open for disruptive innovators taking opportunities to provide targeted services to “traditional system” patients at much lower costs and with equivalent or better outcomes, as well as a better patient experience.

What’s Next

Each system must understand the levers in its own market, as timing and prioritization will be different in competitive urban and suburban areas compared to sole-provider regions, as well as depend on what the current payer environment is doing in encouraging greater provider risk.

Think You’re in the Clear? Think Again.

Even seemingly secure areas will begin to slip as retail clinics, telemedicine provided by disruptors, and employer-driven initiatives to reduce cost drive business elsewhere. By carefully assessing these competitive risks and understanding the variables in their own markets and populations, today’s health systems can begin to define their paths to patient centricity and value transparency in their plans to compete effectively.

Planning Your Health System of the Future

In practical terms, this will require a survey of the current state of affairs for the system to assess its vulnerabilities, followed by a targeted strategy to move the organization across seven key dimensions that enable the delivery of transparent and patient-centric care: care model, provider network, financial

capability, facilities and service distribution, governance and management, workforce, and technology. The challenge is that most systems will need to take an evolutionary approach, requiring sustained commitment and leadership, led by a clear vision of what that system should look like going forward to be successful in its market. Prioritizing where to focus valuable resources for the earliest and most effective returns on the investment will be crucial.

Footnotes

1. Health Care Advisory Board interviews and analysis.

2. A. Mehrota et al., “Visits to Retail Clinics Grew Fourfold from 2007 to 2009, Although Their share of Overall Outpatient Visits Remains Low,” Health Affairs (August 2012).

3. “Oregon insurance regulators took Zoom Health Plan into receivership after they ‘became aware of a material difference between the company’s 2016 annual financial statement and its actual financial condition.’” Oregon Business News (April 24, 2017).

4. “How Much Will It Cost? How Americans Use Prices in Health Care,” a report by Public Agenda with support from the Robert Wood Johnson Foundation (March 2015).

5. H. Sweetland Edwards, “What Happens When Doctors Only Take Cash,” TIME Health (January 26, 2017).

6. ClearBalance Healthcare Consumerism survey (Lavin Entrepreneurship Center at San Diego State University, August 2017), http://www.clearbalance.org/patient-loan-program-drives-loyalty-for-healthcare-facilities.