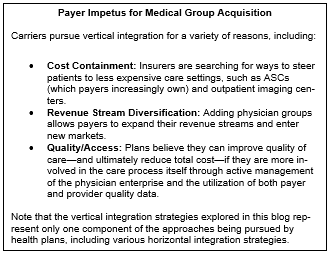

The market for healthcare providers is currently experiencing a tectonic shift as large insurance companies such as UnitedHealthcare/Optum and Humana employ physicians and other healthcare providers in markets across the country. Health systems increasingly find themselves in competition with payers (and private equity firms) to grow their physician networks; medical group M&A activity growth outpaced general healthcare M&A activity growth by 25% from 2014 to 2019. [1]

The COVID-19 pandemic is likely to accelerate this trend. Economic downturns inevitably lead to the consolidation of distressed assets; expect financially stressed physician group practices to seek out partners at a time when health systems are likewise financially challenged. Health plans with excess capital are currently well positioned to acquire providers and will likely grow their networks in the coming months and years.

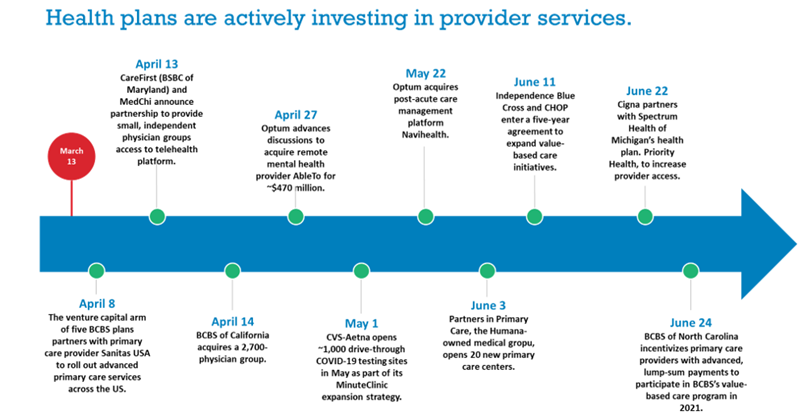

In 2020, this process has accelerated. Optum, Humana, Anthem, Cigna, and other regional providers have acquired or developed large provider groups in select markets, primarily in Washington, California, Texas, and Florida (Optum is now the largest employer of physicians nationwide at nearly 50,000 through its various entities).

Notably, the Optum-backed Polyclinic in Seattle (a 200-physician multispecialty group) recently enticed several productive, experienced primary care physicians to terminate their employment relationships with the nonprofit Swedish Health System. The Polyclinic offered the physicians lucrative compensation packages to make the switch.

Health System Strategies

Payers haven’t yet entered all major markets; however, health system executives need to be prepared to respond to increased competition from payers, and we recommend they consider the following strategies:

For protecting your existing physician assets:

- Review physician compensation to identify at-risk providers. Leading physicians will likely be targets for health plan acquisition; identifying which providers are underpaid relative to their production levels will be critical to protecting these assets.

- Improve operational efficiency and financial performance, thereby enabling providers to boost their compensation through increased productivity or gainsharing. Improving operational efficiencies also enhances financial performance, allowing hospitals to increase physician compensation relative to market and dissuade providers from pursuing other opportunities.

For protecting existing volume/margins:

- Accept value-based risk and improve your relationship with payers moving into the provider space. Pursuing value-based arrangements with payers will further align incentives and allow the hospital to share in some of the gains from their strategy to reduce utilization.

- Enhance your low-cost sites of care to attract additional patient volume, including the pursuit of an ASC strategy, ASC migration analysis, non-HOPD imaging entity, and other cost-reducing efforts. As payers will inevitably push patients to lower-cost settings, ensure your hospital has low-cost alternatives to keep this volume in the system.

- Focus contracting efforts on the other insurers in the market to improve rates and secure their volume. Hospitals can also shift focus to the other leading payers in the region to improve performance on their plan in either volume or reimbursement.

For medical groups that you’d like to remain independent:

- Consider a professional services agreement partnership for select (or all) clinical services. This type of arrangement provides a close linkage while allowing the group to maintain a degree of autonomy.

- Update provider need assessments to identify specialties that the hospital may need to expand in the coming years, and consider employment/increased alignment with these providers to further growth strategies.

- Offer nonproduction incentives to improve quality and performance of other key strategic initiatives (potentially through a comanagement agreement). Hospitals can also increase these groups’ compensation for quality-of-care improvement and program development.

Footnotes

1. Irving Levin Associates Health Care Quarterly M&A Report and Bloomberg BNA Health Law & Business News.